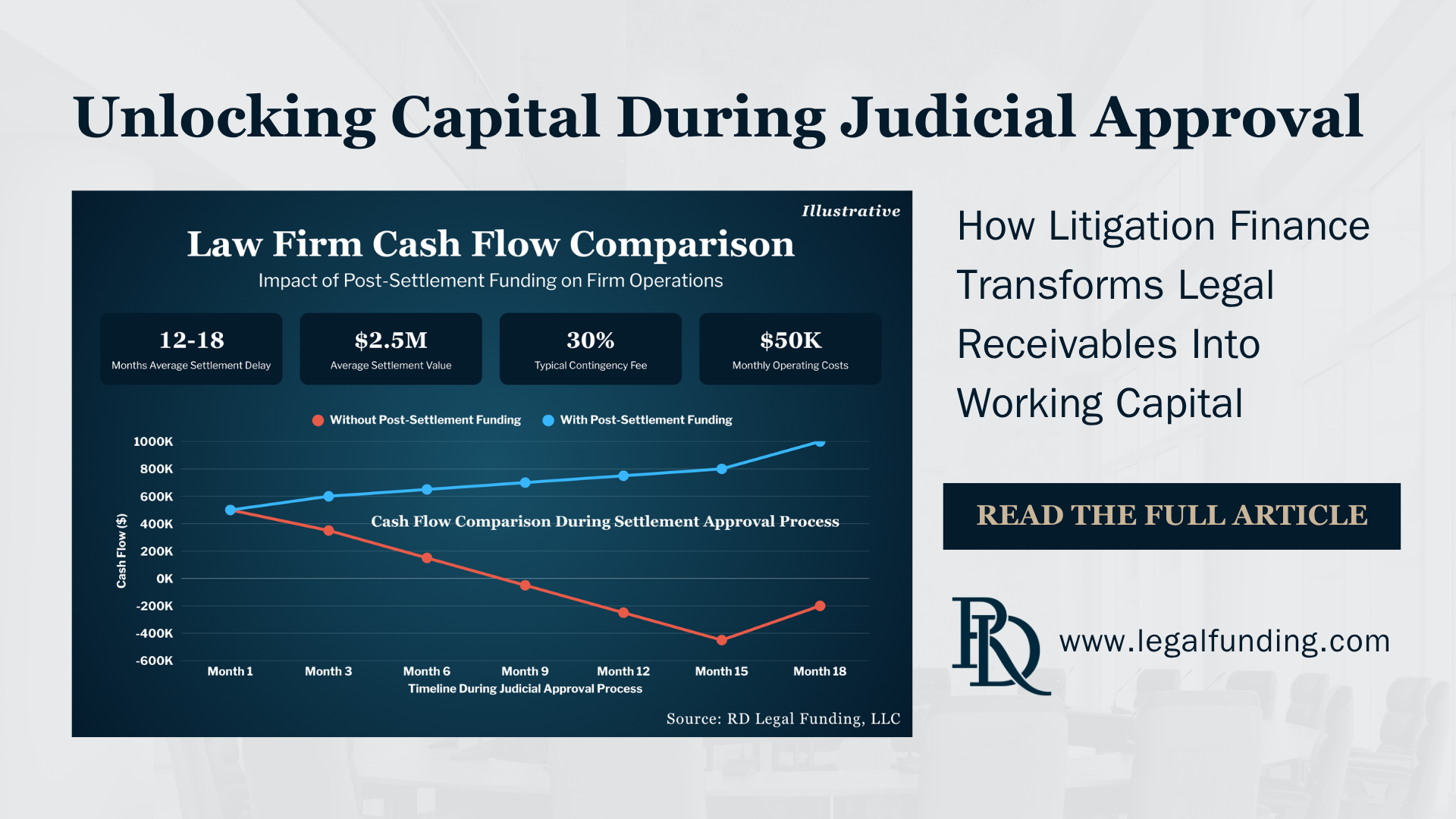

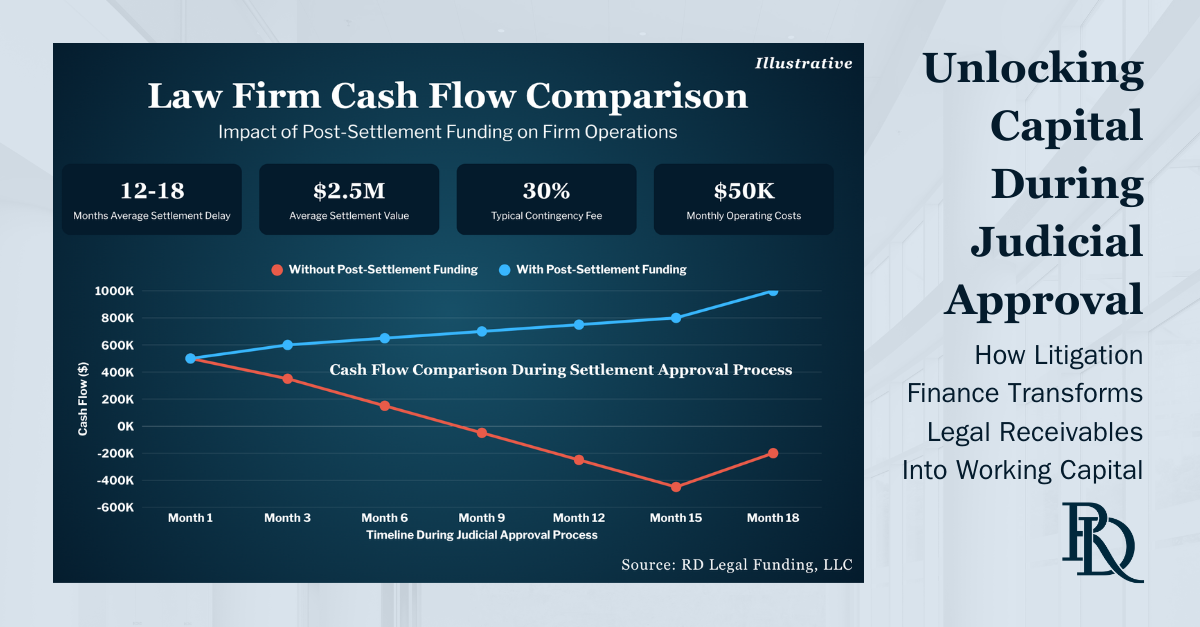

Why Waiting for Probate Could Be Costing Your Law Firm More Than You Think

The numbers are staggering: according to the National Association of Probate Judges, the average probate process takes 6 months to over 2 years to complete, leaving law firms waiting indefinitely for earned fees from settled cases. For senior partners managing firm operations and cash flow, this delay represents a hidden cost that can significantly impact business stability and growth opportunities.

.png)

.png)

.png)